Every year, usually in November, I write a column for clients, advisors and my loyal monthly e-newsletter readers called (2026), Health Insurance State of the Union!

One of the many things that makes Intelisano & Associates, Inc., different, is that we teach you how insurance companies think and make money! Insurance companies thrive when the public is confused! Once our client (the consumer) understands how insurance companies think, there is what I call “The Visine Effect,” when everything becomes clearer and personal decisions are easier to make.

Before getting into the nitty gritty of 2026 health insurance, some facts need to be understood about how insurance works and how insurance companies think:

EVERY insurance company decision is made to AVOID “Adverse Selection!”

Examples of adverse selection:

A. A 22-year-old man paying the same health insurance premium as a 62-year-old man.

B. A heavy cigarette smoker paying the same life insurance rate as a non-smoker at the same age.

Each state is different. For example:

New York State is Community Rated, meaning a 22-year-old woman pays the same rate as a 62-year-old woman. This means there is “Adverse Selection” built into the NYS model!

New Jersey is Age and Experience Rated, meaning a 22-year-old woman pays LESS premium than a 62-year-old woman, and it’s also based on the past 12 months of claims experience.

Health insurance companies assume that almost everybody is sick and they need to protect themselves from “Buying a Claim!”

An example of “Buying a Claim” is an individual with no health insurance and pre-existing conditions buying a new individual policy on their home State Exchange to submit a claim the first 30–60 days! With individual health insurance there is NO protection from “Adverse Selection” for the insurance carrier.

This is why they offer BETTER valued policies at better rates for groups!

For example: A new law firm with 10 employees needs health insurance in New York State and decides to apply with Oxford/United Healthcare. Oxford has PROTECTION from “Adverse Selection” in this group because Oxford uses “Participation Requirements”—60% of eligible employees MUST enroll!

Oxford knows there will be 1 or 2 unhealthy employees that will probably “Buy a Claim.” However, with a 60% minimum participation rate, Oxford will have 4 more employees paying premiums to spread out their risk amongst 6 people! The bigger the group, the less risk for the insurance company, which is why bigger companies pay less.

We have a strategy where a small business can connect to a larger company (pool) to get less expensive policies and better value for the premium. More on that later in Solutions!

Because New York State is Community Rated (age 22 and 62 pay the same) there is “Adverse Selection” built into the NYS model. This is why health insurance carriers “don’t want” this business.

This is why they have removed ALL PPO plans (in and out of network plans) from the New York State (NYS) marketplace, and this is why health insurance carriers have REMOVED commissions for brokers.

No broker commission means fewer policies written and fewer advocates—leaving the public “exposed and confused,” just the way insurance carriers thrive!!

Individuals, sole proprietors and small business owners are in a quandary like never before. Why?

Based on the current timeframe, Congress will be voting twice: once in mid-December to extend Health Insurance subsidies through January, and a second time in mid-January to decide on extending the subsidies (tax credits) for the rest of 2026 or not!

Individuals, sole proprietors, S corporations and employees whose company does NOT sponsor a group health plan must choose a plan based on a subsidy (tax credit) that might only be there for 1 month. Then the premiums go way up starting on February 1st through year-end!

How do you pick a plan with NO premium guarantee?

I decided to take this a step further (we don’t do business with the exchanges/marketplaces) and went onto the NYS marketplace and plugged in some numbers.

A. A New York–based family of 4 making $100,000 receives $905/month of subsidy. That is $10,860 per year; however, it is more than that! This family, if paying the $905 per month extra on their own, would have to make well over $1,000 per month to NET the $905 after taxes.

B. A NYS individual making $60,000 gets $370 per month in subsidy.

Are they removing 100% of the subsidy and how do I know how it affects me?

It is based on income and size of family. The FPL (Federal Poverty Level) for 2025 is:

Small groups are the backbone of this country. Usually, health insurance benefits are their 3rd largest cost, after rent and salaries.

Oxford/United Healthcare (they are the same company) has over 70% of the small business market in New York. UnitedHealthcare policyholders will have a 6.8% premium increase as of January 1st, 2026.

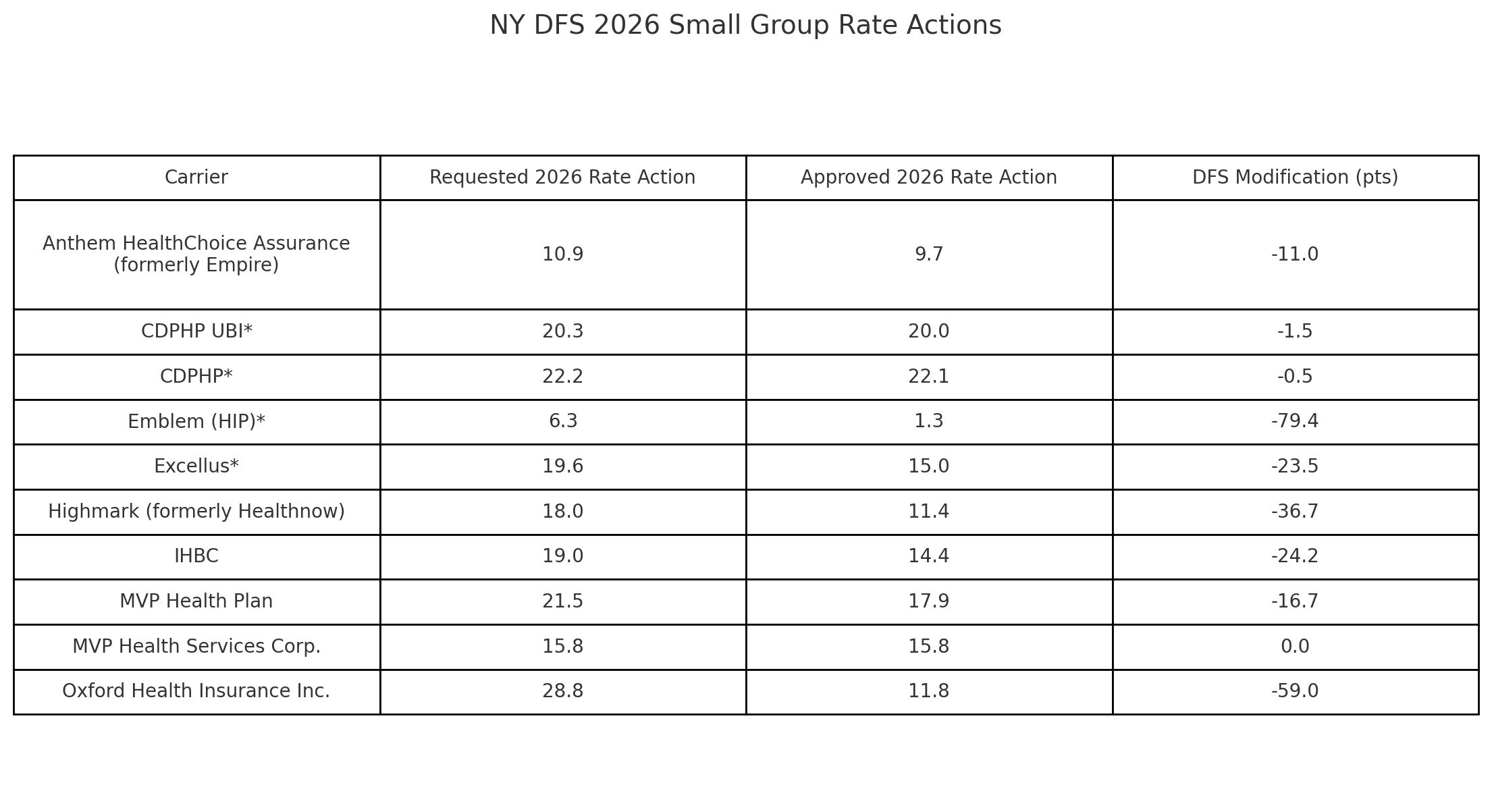

On September 3, 2025, The New York State Department of Financial Services (DFS) announced the final rate increases for small groups in the 2026 plan year.

Insurers requested an average rate increase of 24.0% in the small group market. DFS cut this average rate increase to 13.0% (a 45.8% reduction).

“We have Oxford/United Healthcare and the premiums have gotten outrageous. My broker says there are no other options. What can we do?”

Call your health insurance broker and ask for alternatives. If none…

Call The Insurance Doctor now or later, as we have access to a plethora of non-Obamacare health plans with networks such as the Cigna Open Access Network and the PHCS Multi-Plan network, more reasonably priced—and you can switch into them mid-year.